Usually, financial problems do not stem from one major disaster. In most cases, financial problems creep into our lives quietly over time they may hurt us later. We will discuss the 11 biggest financial mistakes that people make and how one can avoid them to secure their future.

At Financier Mind, our aim is not to judge people’s financial decisions. We aim at creating awareness. Everyone is prone to making financial mistakes at some point. What separates financial problems from financial stability is the ability to learn from our mistakes.

Why Understanding Financial Mistakes Matters

The consequences of a financial mistake are not just limited to money; they are also related to relationships, stress, life opportunities, and wealth accumulation.

The consequences of a financial decision gone wrong are:

- Long-term debt

- Investment opportunities lost

- Loss of financial freedom

- Emotional stress and anxiety

Here are common money mistakes that hurt finances.

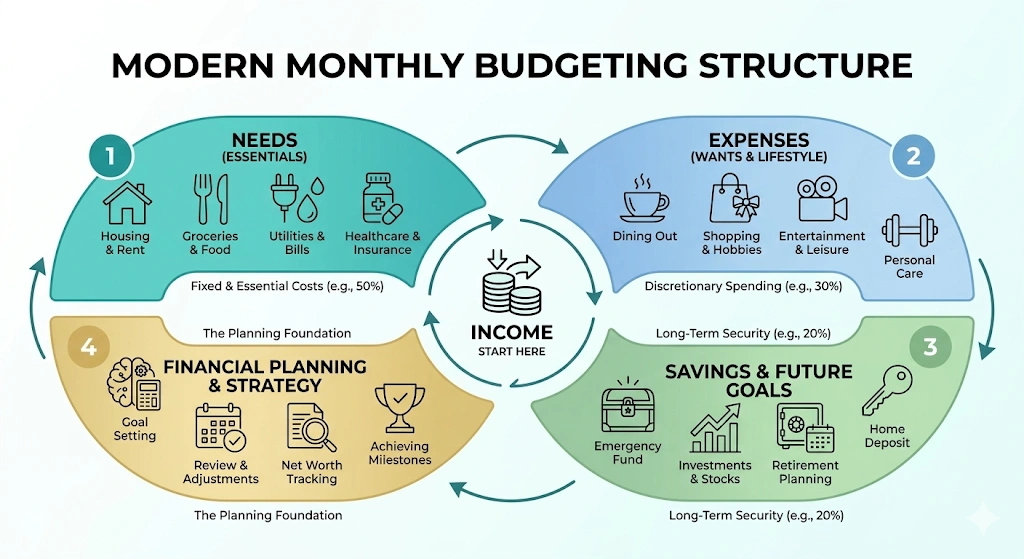

1. Having No Budget

Lack of a budget is one of the most common financial blunders.

It is a common perception that a budget is a constraint. However, in reality, a budget helps in gaining awareness about how to utilize money in a better way.

Lack of a budget results in:

- Increasing expenses

- Erratic savings

- Easier debt creation

Real-Time Example

Imagine a person earns a salary of ₹60,000 per month. The person might thinks he is financially secure. However, without a budget, he might end up spending his whole money on various things, and at the end of the month, there will be zero money left for saving.

Simple Solution to Budgeting

A person needs to follow a monthly pattern in terms of:

- 50 percent needs

- 30 percent lifestyle spending

- 20 percent saving

2. Impulsive Spending Habits

Impulse buying is another silent financial blunder.

Today’s advertisements promote impulsive spending. Shopping apps and credit cards have made it easy to buy things online.

Impulsive spending results in:

- Regret purchases

- Increased credit card debt

- Reduced savings potential

Practical Tip

If you are about to buy something costly, follow this 48-hour rule:

If you still need it after 48 hours, it’s probably a rational purchase.

3. Having No Emergency Fund

Life is unpredictable. A medical emergency, loss of job, or unexpected expenses can occur at any given moment of Life.

If an individual does not have an emergency fund, then he/she may have to resort to:

- Using credit cards

- Taking personal loans

- Seeking loans from friends or relatives

This will only add to more stress.

Ideal Emergency Fund

According to financial planners, it is advisable to set aside 3 to 6 months worth of living expenses. This fund should not be part of the investment fund.

4. Marrying the Wrong Person

However, the aspect of financial compatibility in relationships is often not taken into account, yet it plays an important role in the stability of relationships.

Financial compatibility issues include:

- Differences in saving habits between two people, with one person saving money while the other spends it lavishly

- Differences in opinions about debt repayment and investment strategies

- Differences in opinions about financial planning strategies

Financial communication in relationships before tying the knot can prevent future problems.

5. Taking a Loan for a Wedding

For many societies & Culture , a wedding can be a very expensive thing in their lives which can cause their whole savings.

It can be the big expense for something that only lasts a few days.

Consequences

- Long repayment periods

- Reduced financial flexibility

- Delayed financial goals

A wedding is supposedly to celebrate a relationship between the former couples , not put a strain on their finances.

6. Getting Into Credit Card Debt

Credit cards, though useful, become dangerous when abused.

One of the worst financial blunders a person can make is to have credit card debt.

Credit card interest rates tend to be extremely high.

Example

For instance, if a person uses a credit card to buy something worth ₹50,000 and then only pays the minimum, the interest added to the bill may build up over time.

The consequences of a credit card debt can lead to a purchase turning into a debt over a period of time.

Smart Practice

Always settle your credit card bill in full before the due date.

Understand how credit card works.

7. Not Having Enough Insurance

Insurance helps to protect against major financial shocks.

However, it is unfortunate that many people tend to pay little attention to insurance unless something goes wrong.

There are two main forms of insurance:

- Health Insurance

- Life Insurance

8. Buying a Home You Cannot Afford

The purchase of a house is often regarded as a status symbol. However, the purchase of a house beyond financial capability is risky. The amount spent on a house as a monthly mortgage must ideally be below 30 to 35 percent of the income.

If the expenses of a house consume most of the income:

- Savings become hard to achieve

- Flexibility in life ceases to exist

- Stress begins to build up.

A home should create stability it should not create any kind of pressure.

9.Having Only One Source of Income

Being dependent solely on a single source of income is no longer a safe bet.

Economic changes, company layoffs, or industry changes may affect job security at a large scale.

Having multiple sources of income makes a person financially secure.

Multiple sources of income streams provides financial resilience.

Examples Includes:

- Freelancing

- Online businesses

- Investments

- Rentals

Diversification strengthens financial security.

10. Buying a Car Out of Your Price Range

Cars depreciate quickly.

Over-spending on a car can influence one’s savings and investments.

People buy luxurious cars due to peer influence rather than its financial viability.

Smarter Approach

The best option for a car is to buy one that costs less than half the annual income.

Transportation should not be expensive to allow for wealth creation.

11. Expensive Vacations You Cannot Afford

Travel experiences are valuable, yet going into debt to finance these experiences can cause stress in the near future.

Some people take debt to finance their luxurious trips.

This leads to:

- Debt after the trip ends

- Interest payments

- Lack of flexibility

Vacations should be well within the means of those taking the trips, not going into debt.

The Hidden Pattern Behind Financial Mistakes

The majority of financial blunders tend to follow a similar pattern.

They are often the result of prioritizing short-term comfort over long-term security.

Examples Include:

- Indulging in immediate comforts

- Emotional spending

- Giving in to social pressure

Recognizing this pattern helps avoid repeated financial mistakes.

Building Financial Discipline

Avoiding financial mistakes requires simple but consistent habits.

Key Practices Include:

- Tracking Expenses

- Having Emergency Savings

- Avoiding Unnecessary Debts

- Investing Regularly

- Planning major Expense carefully

Financial discipline grows gradually.

Long Term Financial Awareness

Money decisions today shape future possibilities.

Avoiding common financial mistakes allows people to:

- Builds wealth steadily

- Reduces financial stress

- Maintain Independence

- Create opportunities for the future.

Small improvements today can lead to significant better long-term results.

Final Verdict

However, the difference lies in the lessons one learns from the mistakes.

Avoiding the above 11 financial mistakes not only ensures the safety of one’s savings but also ensures a better financial future.

The first step towards financial wisdom is to be aware.

FAQ’s

1. What is the most common financial mistake?

- Living without a budget

- Overspending without tracking expenses

2. How much emergency fund should I have?

- Minimum three months of expenses

- Ideally six months of living costs

3. Is credit card debt dangerous?

- Yes, High interest rates make repayment difficult, If not paid on time

4. Why is insurance important for financial planning?

- Protects against large unexpected costs

- Prevents savings from being wiped out

5. Can avoiding financial mistakes help build wealth?

- Yes, Wealth grows when financial leaks are eliminated